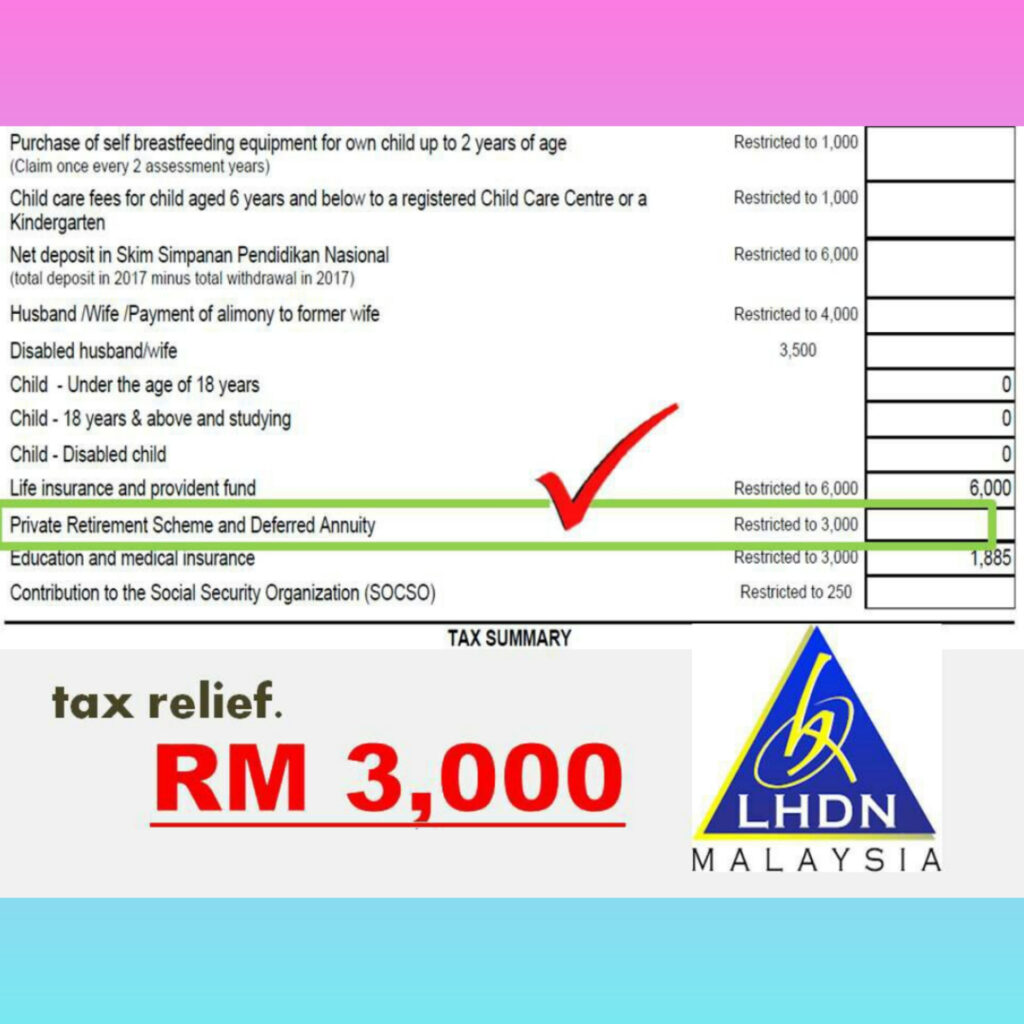

What is PRS in Malaysia?

Private Retirement Schemes (PRS) is a voluntary long-term savings and investment scheme designed to help you save more for your retirement. PRS seeks to enhance choices available for all Malaysians whether employed or self-employed to supplement their retirement savings under a well-structured and regulated environment.

私人退休金计划(PRS)是一项自愿性长期储蓄与投资的计划,特为个人累计退休储备金而设。 PRS 为所有受雇或自雇的马来西亚人民提供多一个选项,以便在这个架构完善且受监管的环境下补足他们的退休金。人们可从 PRS 基金管理公司所提供的各项退休基金中,依据个人的退休需求、目标和风险承受度来决定他们的投资。这些 PRS 基金选项主要让会员在这个受良好监管的框架下提高投资人士的长期回报。

WHY SHOULD I SAVE MORE?

- Studies and reports recommend having at least two-thirds (67%) of your last-drawn income to maintain your current living conditions when you retire.

- To achieve the two-thirds benchmark for your retirement, PPA suggests saving a minimum of a third (33%) of your monthly salary.

- In the private sector, one can assume you are already contributing 11% of your salary to a mandatory scheme, while your employer contributes 12%, bringing mandatory contributions to a total of 23%.

- Hence, you only need an additional 10% of your monthly income in Private Retirement Schemes (PRS) to get more out of life when you retire.

- 研究和报告建议您在退休时至少拥有您最后所领薪资的三分之二 (67%)以维持您现有的生活条件。

- 为了达到退休收入的三分之二基准, PPA建议您每个月至少将薪资的三分之一(33%)储蓄起来。

- 如您在私人机构工作,则可假设您已经将月薪的11%存入强制性储存计划,加上您的雇主缴纳12%,因此强制性存款总额已达23%。

- 因此,您只需将月薪额外的10%储蓄与投资在私人退休金计划(PRS),以便在退休后享受更好生

WHY DO I, SAVE IN PRS

How Does the Scheme Work?

Regardless of the option chosen, your contributions will be maintained in two separate sub-accounts as follows:

无论选择哪个选项,你的贡献都将保留在两个独立的子账户中,如下所示:

PRS ACCOUNT

*1You are eligible to make full withdrawal upon reaching the age of 55. Securities Commission Malaysia may specify any other age from time to time.

在达到55岁时,您有资格进行全额提款。马来西亚证券委员会可能会不时规定其他年龄。

*2Subject to terms and conditions.受条款和条件约束。

Enroll or Top Up your PRS here now!